Market volatility and recession fears force many organizations to better control (and continuously improve) costs.

One of the first things executives turn to for cost improvement projects is benchmarking.

Benchmarking can come in many forms: qualitative and quantitative, and internal and external. For purposes of this article, we’ll focus on pros and cons of benchmarking your costs against peers (e.g., other companies in the same industry and/or of similar size).

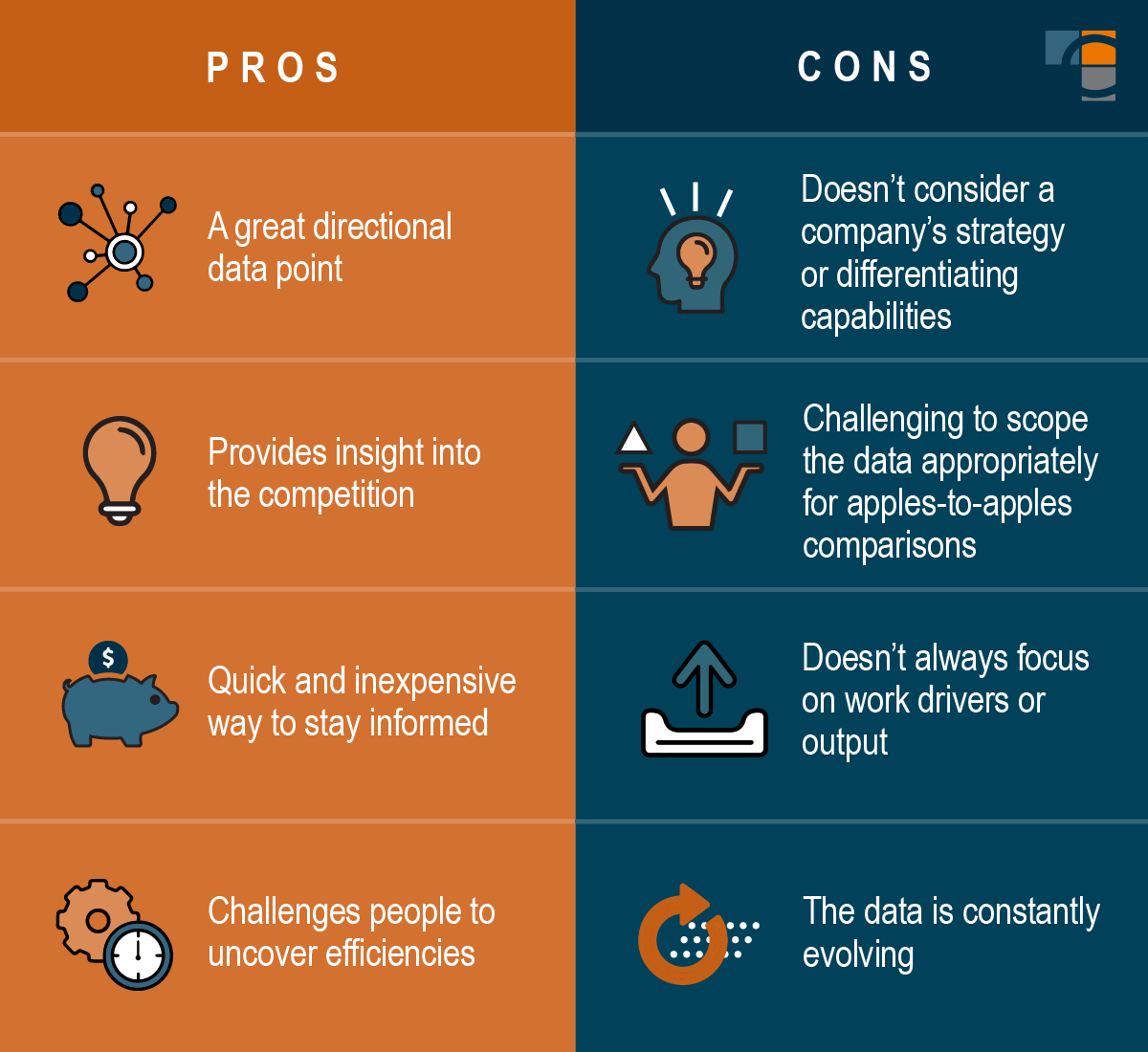

Pros

A great, directional data point.

Cost benchmarking gives you transparency into the competitive landscape – it tells you where you stand. You may see that your total G&A costs as a percentage of revenue are 20% higher than the top quartile of the data set. That at least gives you actionable insight to examine your costs and try to understand what is driving the difference.

Functional (e.g., HR, Finance, Operations, IT) cost benchmarking can direct you to where the gaps may be – it tells you where to prioritize efforts.

Provides insight into competition.

We live in a more transparent world, but competitors can still be a black box. Benchmarking tells you how those companies are prioritizing costs, which could help you infer strategic decisions. A better understanding of competition can lead to idea generation for internal improvements.

Quick and inexpensive way to stay informed.

Continuous cost improvement is critical to sustainable growth. Part of staying on top of your cost structure is always knowing where you stand versus your peers.

Organizations can typically source benchmarks or participate in industry surveys to constantly assess cost levels versus similar companies.

Challenges people.

A huge factor in successful cost improvement programs is rallying your organization around the mission.

Benchmarks can point to potential gaps and challenge managers to find opportunities for higher efficiency. Deputizing your staff to improve costs creates a two-way dialogue around continuous improvement opportunities and can generate a shared purpose (even crowd-sourcing ideas) across business units at a time when people may be uncertain of the company’s (and their own) future.

Cons

Doesn’t consider a company’s strategy or differentiating capabilities.

There are good costs and bad costs. Good costs are those that add business value or reinforce areas of differentiation. Benchmarking alone doesn’t distinguish between the good and the bad.

For example, Company A may have higher IT costs as a percentage of revenue than Company B, C, and D. However, Company A may be investing in automation that has driven lower labor costs in other functions (e.g., Finance).

Mitigation: Always start with a clear strategy when tackling a cost improvement project and refer back to that strategy as you assess benchmarking data versus other companies.

Challenging to scope the data appropriately to make each company apples to apples.

Every company is structured differently.

One company’s finance function could be centralized, while another has several activities outsourced. If the outsourced cost is not included in the benchmarks, the data will not be apples to apples.

Further, some finance organizations may include non-traditional finance roles like Business Development and Supply Chain (if integrating Order to Cash resources). If these differences are not accounted for in the numbers, there will be a mismatch.

Mitigation: Always use a trusted partner for benchmarking data, make sure that provider clearly explains the scope of the peer set data, and take time dissecting and understanding the results.

Doesn’t always focus on work drivers or output.

The most widely used cost benchmark is cost as a percentage of revenue. Why? Because every company has revenue, and it’s the most obtainable comparison.

However, revenue isn’t always synonymous with what drives the work. Using IT again as an example, comparing costs against the number of applications managed can be much more effective – albeit harder data to obtain.

Cost benchmarks also don’t focus on productivity or output. As mentioned above, cost is not synonymous with value delivered. One company’s HR department could be higher cost, but that HR department could be instrumental in bringing in and developing talented business professionals.

Mitigation: If available, seek benchmarks that focus on what drives the work for that particular function in addition to traditional revenue benchmarks.

The data is constantly evolving.

Benchmarking, like many data points, is at a specific point in time. As markets change and companies evolve, benchmarks (and benchmark data) will change. Consequently, historical data during historical anomalies doesn’t create meaningful comparisons in the benchmarking process.

In a tough economic period, many companies slash budgets. 2020 is a good example – companies slashed costs at alarming rates during the pandemic. Benchmarks in 2020 and soon after are a lot lower than in 2019.

Further, companies continue to get more efficient as technology accelerates. Benchmarks will continue to get lower and lower in many functions.

Mitigation: Always know the time period of the benchmarks and use benchmarking as a data point, not the answer or the target. Instead of zeroing in on the point-in-time benchmark, predict what the future benchmark could be.

The Bottom Line

Benchmarking is a relatively easy way to get data to support decisions in a cost improvement program.

These metrics can produce actionable insight for execs in any industry or organizational size when used with transparency and proper symmetry with other data sets. It’s important that you don’t use benchmarks as “the answer.” Scope them appropriately, and take time dissecting the results to understand what they mean.

To optimize your cost structure with expert strategy, technology, and, most importantly, empathy, contact CrossCountry Consulting today.